Regulatory changes are bringing conditions closer for domestic and foreign companies in e-commerce

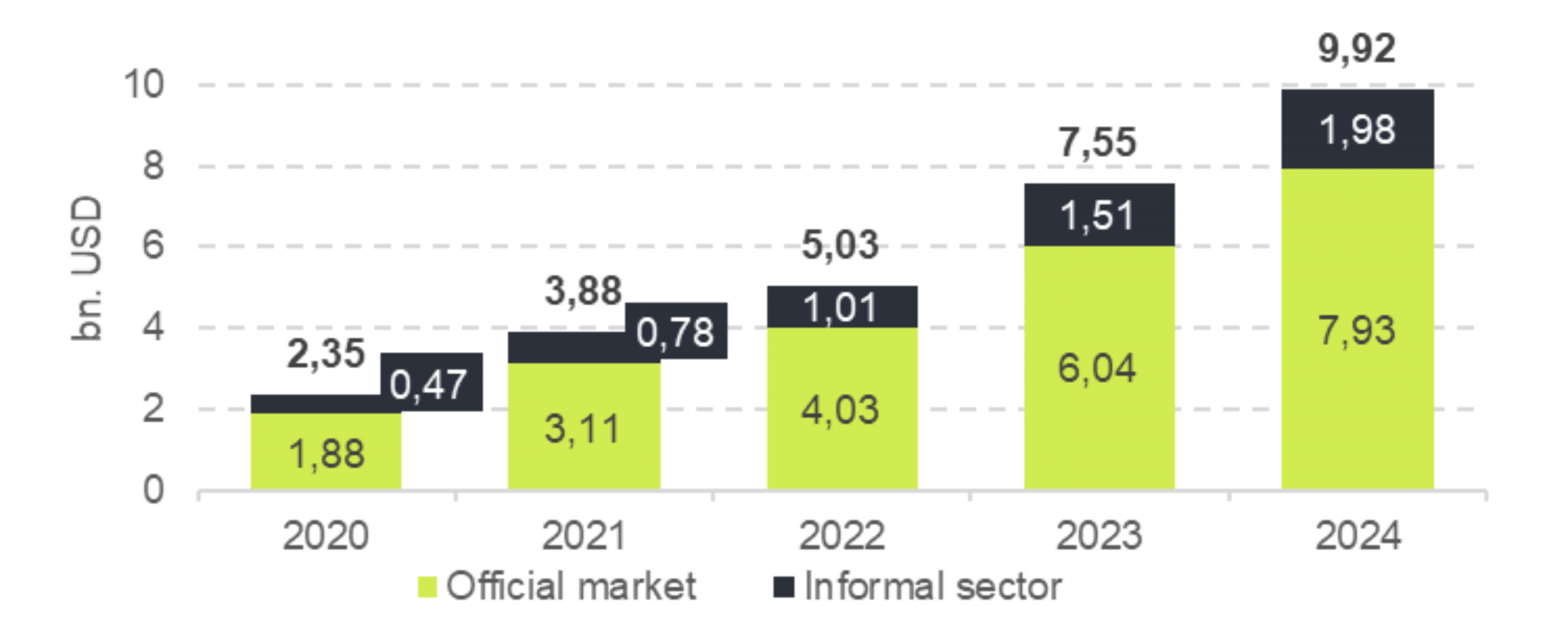

Baker Tilly Qazaqstan Advisory conducts an annual assessment of Kazakhstani e-commerce market and compiles a ranking of online platforms. According to our estimates, as of the end of 2024, the total size of the e-commerce market amounts to approximately USD 10 billion, including the informal segment of the market, which we estimate at approximately 25%.

Dynamics of the e-commerce market size over the period 2020–2024, bln USD

Source: Baker Tilly Research

In light of the upcoming amendments to customs legislation, effective from July 1, 2026, we anticipate an increase in market transparency. These changes may necessitate a revision of the current methodological approaches used to estimate the overall market size.

Traditionally, one of the sources of the informal segment e-commerce has been goods and services from abroad, as they are easier to conduct outside standard reporting. They are more often paid for through foreign payment systems, and parcels are frequently declared as private shipments, making such transactions more difficult to track.

This leads, first, to forgone tax revenues for the budget and, second, to the creation of unfair competitive conditions, as foreign sellers effectively find themselves in a more advantageous position compared to Kazakhstani market participants.

In response, Kazakhstan introduced a value-added tax for foreign internet companies in 2022, informally referred to as the “Google tax.” Since then, companies that sell goods or provide electronic services to Kazakhstani consumers have been required to register as VAT payers and pay the tax at a rate of 12%.

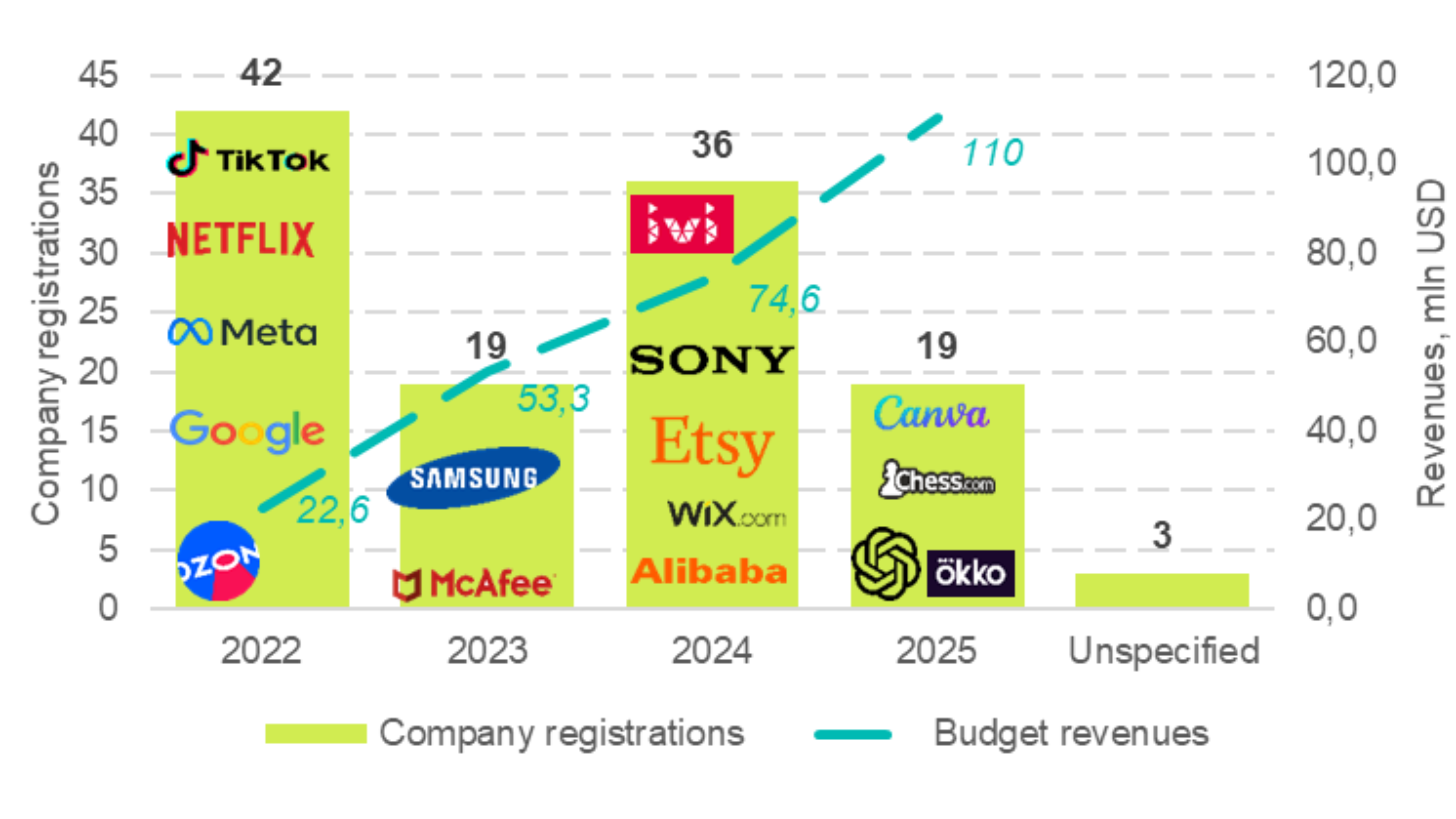

As of the end of 2025, the list of “Google tax” payers included 119 companies, of which 42 were registered in 2022, 19 in 2023, 36 in 2024, and 19 in 2025.

Breakdown of the number of registered “Google Tax” taxpayers by year and revenue dynamics, mln USD

Source: State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan

Among them are both global technology companies (Apple, Google, Meta, Sony), large marketplaces (Amazon, Alibaba, Ozon), and niche services with a narrow specialization, such as the VPN service TunnelBear and the chess platform Chess.com. Against the backdrop of expanded administration, revenues from this tax have increased significantly, from USD 22.6 mln in 2022 to USD 110 mln by 2025.

At the same time, the number of foreign companies actually operating in the market clearly exceeds the number of registered taxpayers. As a result, an imbalance in the tax burden persists. For example, OpenAI has been selling subscriptions to ChatGPT since 2023 but only registered for VAT in 2025. As a result, the law penalizes compliant behavior while effectively encouraging avoidance.

As of January 1, 2026, however, the tax regulator has gained the ability to block the websites of foreign companies that fail to register as VAT payers in Kazakhstan. Concerns that large players might simply ignore these requirements and exit the Kazakhstani market appear weak: if a company already operates in other countries, paying VAT is standard practice for it.

In addition to the “Google tax,” regulation of cross-border e-commerce within the EAEU is also being strengthened. All online purchases from outside the union are being brought under a regime of mandatory customs declaration through e-commerce operators.

Previously, a duty-free threshold of 200 EUR and 31 kg per parcel applied. If exceeded, a 15% duty was charged only on the excess amount, or not less than EUR 2 per kilogram above the limit. From 2026, the EUR 200 threshold remains, but the principle changes: the duty is applied to the full value of the goods, rather than only the excess. The rate is set at 5% of the purchase value, but not less than EUR 1 per kilogram, after which an additional 16% VAT is charged.

This model preserves preferential treatment for low-value purchases while making higher-value orders more expensive. The new approach will also improve the tracking of cross-border flows, enhance market transparency, and reduce opportunities for informal schemes.

In line with the broader tightening of tax control over e-commerce, the new Tax Code introduces specific requirements for marketplaces. Platforms assume responsibility for collecting and remitting VAT on transactions conducted on their platforms, both in domestic and cross-border trade.

This further underscores their infrastructural role. Unlike classifieds, which merely host listings, marketplaces cover key stages of the transaction: they process payments, organize delivery, ensure basic trust between the seller and the buyer, and handle returns and quality control. The new requirements simply add a fiscal function to this role.

A conditional registration mechanism is introduced for foreign sellers, allowing them to register for tax purposes without establishing a legal entity in the country. This makes it possible to tax such sales on terms comparable to those applied to domestic sellers, without driving foreign players out of the market through excessive bureaucracy and additional costs.

Overall, the tightening of regulation across several areas indicates that the e-commerce market has already reached a scale at which it is being regulated in greater detail, including the cross-border segment. For Kazakhstani sellers, this is a positive development, as it reduces the competitive imbalance with foreign players. For consumers, the effect is more mixed. The new rules will inevitably lead to higher prices for foreign goods and services, as part of the additional costs will be passed on to them. In the long term, however, consumers are likely to benefit competition will increasingly be determined by quality, price, and business efficiency rather than differences in tax regimes and the ability to circumvent them This, in turn, will make the market more transparent and sustainable.